Santander is one of the UK's biggest high street banks, particularly popular with small businesses. For lenders operating in the UK market, Santander business statements appear frequently in application packs. Their statements look clean enough at first glance. Then you try to extract the data for an affordability assessment.

Santander business statements have some unique quirks that make them genuinely awkward to parse. Not because the layout is bad - it is actually fairly clean - but because of what they embed around the transactions. For lending teams processing these at volume, these quirks create extraction errors that require manual cleanup.

Marketing in Your Statement

Open a Santander business statement and the first thing you will see is not transactions. It is this:

"News and information." "Beyond banking." A paragraph encouraging the account holder to visit santander.co.uk/business. This is marketing copy, printed directly on the bank statement.

For a human, it is easy to skip past. For a parser, this is noise that sits right where you would expect account data to begin. A generic PDF extraction tool will pull this text out and try to make sense of it alongside the actual transactions. For a lender who needs reliable automated extraction, this means the parser needs to know it is there and deliberately ignore it.

Fee Tables That Look Like Data

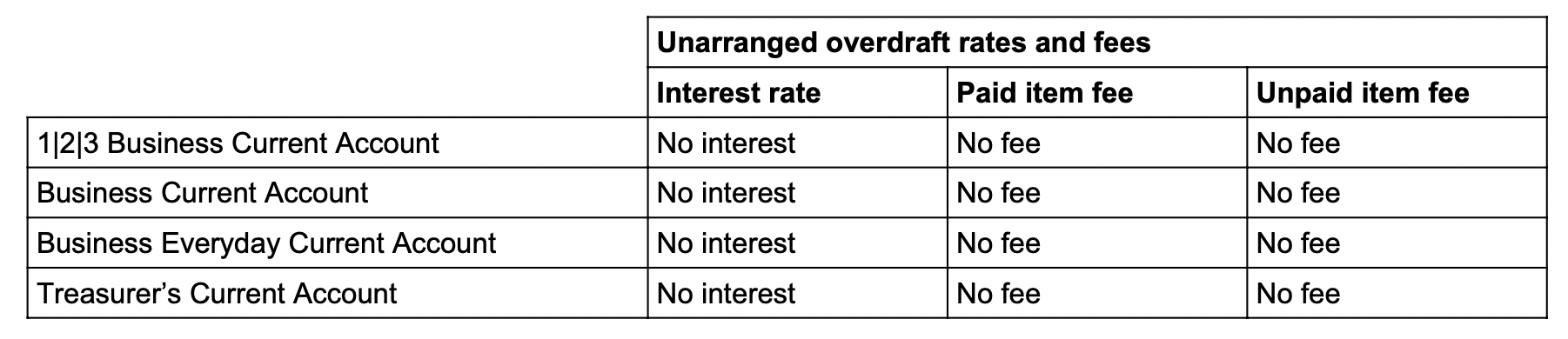

It gets worse. Santander statements also include structured tables like this:

Unarranged overdraft rates and fees. Neatly formatted rows and columns. Account types, interest rates, paid item fees, unpaid item fees. It looks exactly like structured financial data - because it is. It is just not the applicant's transaction data.

This is the kind of thing that trips up AI-based extraction tools. They see a well-structured table and assume it contains transactions. It does not. It is boilerplate terms and conditions that Santander prints on every statement. For lenders relying on automated analysis, a parser that cannot tell the difference between a transaction table and a fee schedule will produce corrupted output that requires manual review - defeating the purpose of automation entirely.

The Previous Statement Balance

When you do find the actual transaction table, it starts like this:

Date. Description. Credits. Debits. Balance. Clean column headers. Then the first row: "Previous statement balance" with a balance of 12,401.17. No date. No credit or debit amount. Just a starting position.

This is not a transaction - it is context. Include it in the extracted data and it will throw off anyone trying to sum the columns or calculate net cash flow. Exclude it carelessly and you lose the opening balance, which is essential for verification. A lending platform needs to handle this as metadata, not as a transaction row. It is the same pattern seen in Barclays statements, and it requires the same careful handling.

Transactions Without Balances

Here is the one that is easy to miss:

"INTEREST PAID AFTER TAX 0.00 DEDUCTED" - a credit of 3.13. But look at the balance column. It is empty. No running balance for this transaction.

Most Santander transactions include a running balance, but not all of them. Interest payments, charges, and certain system-generated entries can appear without one. If a parser expects every row to have a balance, it will either crash or silently misalign the data that follows. For a lender processing dozens of Santander statements daily, this kind of silent data corruption is particularly dangerous because it may not be caught until much later in the underwriting process.

The parser needs to handle missing balances gracefully - carry forward the previous balance, calculate from the transaction amount, or flag the gap. What you cannot do is assume every row is complete.

Ordinal Dates

One more detail. Look at the date format: "3rd May". Not "3 May" or "03/05". Santander uses ordinal suffixes - 1st, 2nd, 3rd, 4th, and so on. And like most UK bank statements, there is no year.

Most date parsers handle "3 May" just fine. Fewer handle "3rd May" without choking on the suffix. It is a small thing, but small things add up when you are processing hundreds of pages across thousands of lending applications.

Why Santander-Specific Logic Matters for Lenders

Santander statements are not ugly. They are not formatted like HSBC's mainframe output or laid out in landscape like Starling. They look reasonable. The difficulty is that the actual transactions are buried between marketing content, fee schedules, and informational tables that a parser needs to navigate around.

It is not enough to find and extract a table. You need to find the right table, skip the non-transaction rows, handle missing balances, and parse dates with ordinal suffixes. Every Santander statement has these challenges, and given how popular Santander is with UK small businesses, lenders will encounter them regularly.

ExactSum's Santander-specific parsing logic handles all of these edge cases. Marketing content is filtered out. Fee tables are identified and skipped. The previous statement balance is captured as metadata. Missing running balances are handled gracefully. Ordinal dates are parsed correctly. What your lending team receives is clean, structured transaction data ready for affordability analysis.

See How ExactSum Handles Santander Statements

Santander-specific parsing built for lending teams who need reliable data extraction at scale.

Book a Demo