Chase is the largest bank in the United States. More business checking accounts than anyone else. When your lending team receives financial documents from applicants, there is a strong chance a Chase statement will be in the stack. Their statements are bold, blocky, and confident - big section headers, clean dividers, plenty of whitespace. They look like they come from a bank that has its act together.

Then you try to extract the transaction data programmatically for an affordability assessment, and you realise Chase does things very differently from other banks. For lending teams processing high volumes of applications, these quirks can lead to extraction errors, manual rework, and delayed decisions.

Page One: Fee Notices, Not Transactions

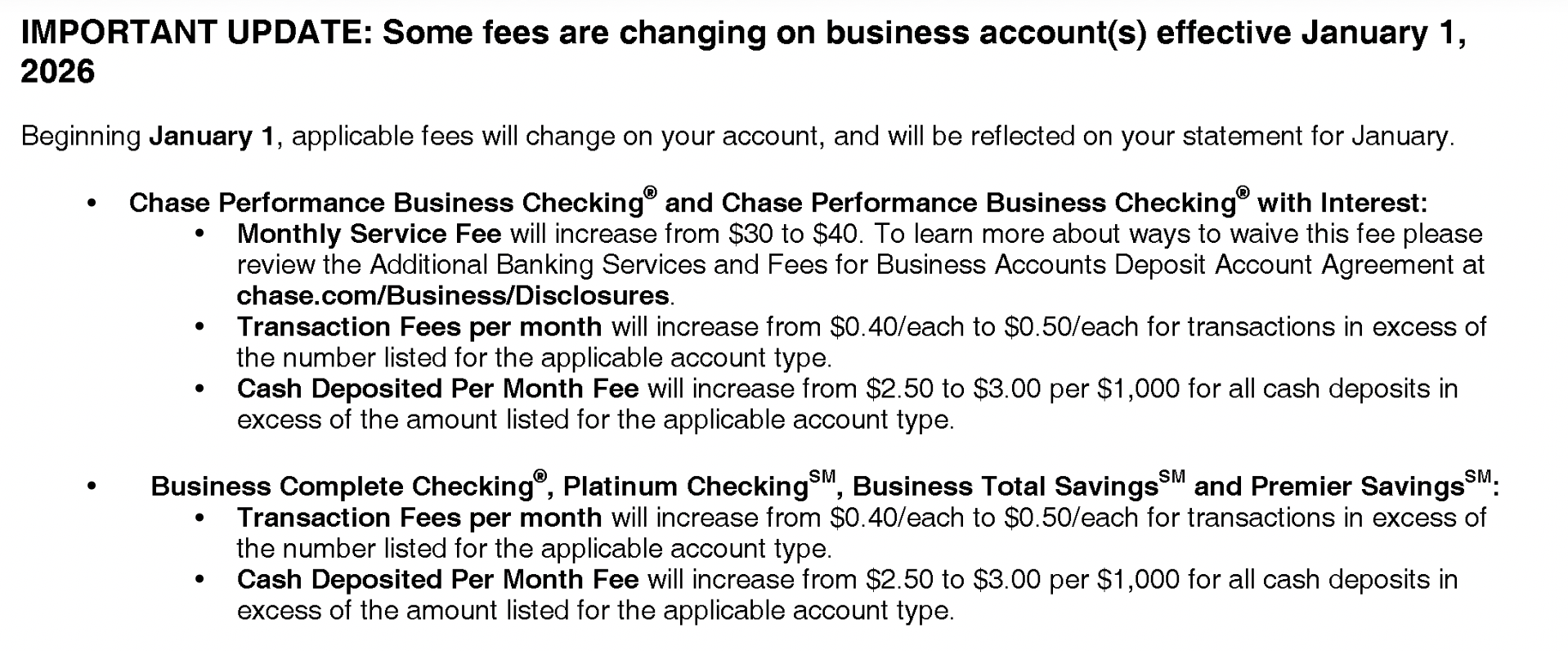

The first thing a parser encounters on a Chase business statement is not account data. It is this:

"IMPORTANT UPDATE: Some fees are changing on business account(s)." Then bullet after bullet of fee increases, policy changes, and references to chase.com/Business/Disclosures. Dense, nested text with trademark symbols and superscript marks scattered throughout.

For automated extraction, this is a minefield of unstructured text sitting exactly where you would expect useful data to start. It is not a table. It is not transactions. It is legal notices that happen to contain dollar amounts like "$0.40/each to $0.50/each" - numbers that could easily be mistaken for transaction amounts by a generic AI extraction tool that does not understand the difference. When a lender needs clean transaction data for income verification, this kind of noise can corrupt the entire output.

The Checking Summary

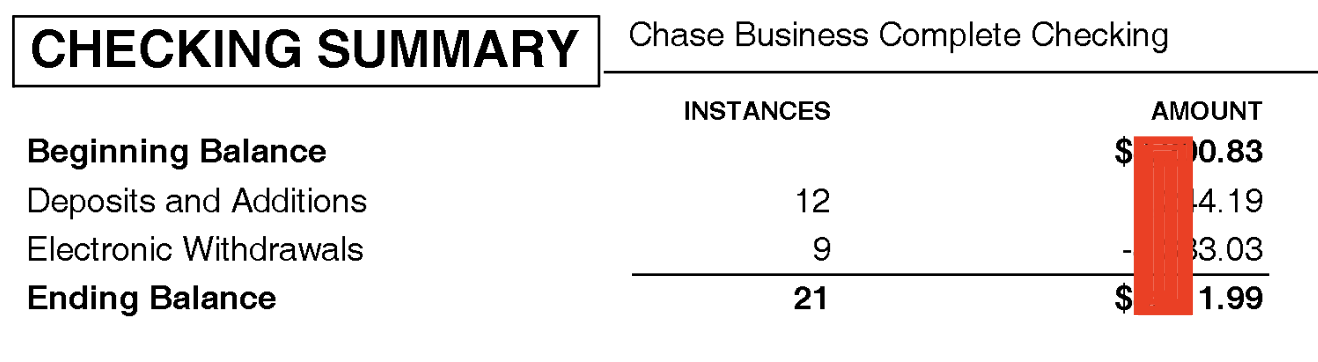

Scroll past the notices and you find the account summary:

CHECKING SUMMARY. Beginning Balance. Deposits and Additions. Electronic Withdrawals. Ending Balance. Chase even tells you the number of instances - 12 deposits, 9 withdrawals, 21 total. For lending analysis, this is genuinely valuable.

A well-built parser can use these numbers as a verification layer. Extract all the transactions, count them, and compare against the summary. If you found 20 transactions instead of 21, you know something was missed. For lenders who need to trust the data feeding their credit decisions, this built-in cross-check is critical. Not every bank provides it.

Credits and Debits: Separate Worlds

Here is where Chase really diverges from the norm. Most banks present transactions in a single chronological table - date, description, money in, money out, balance. One table, everything in order.

Chase does not do that. Credits and debits live in completely separate sections:

"DEPOSITS AND ADDITIONS" is its own section with Date, Description, and Amount. Then separately, "ELECTRONIC WITHDRAWALS" with the same columns. Two distinct tables, two distinct sections.

For a lender trying to build a chronological cash flow picture of an applicant, this structure creates real problems. You cannot just extract one table. You need to extract both tables, tag each row as a credit or debit, merge them together, and sort by date. That is extra logic that most generic PDF tools do not handle - and getting it wrong means your affordability assessment is based on incomplete or disorganised data.

And notice: there is only an Amount column. No separate columns for credits and debits. No running balance. Just a date, a description, and an amount. You have to know which section you are in to determine whether that amount is money coming in or going out.

No Running Balance

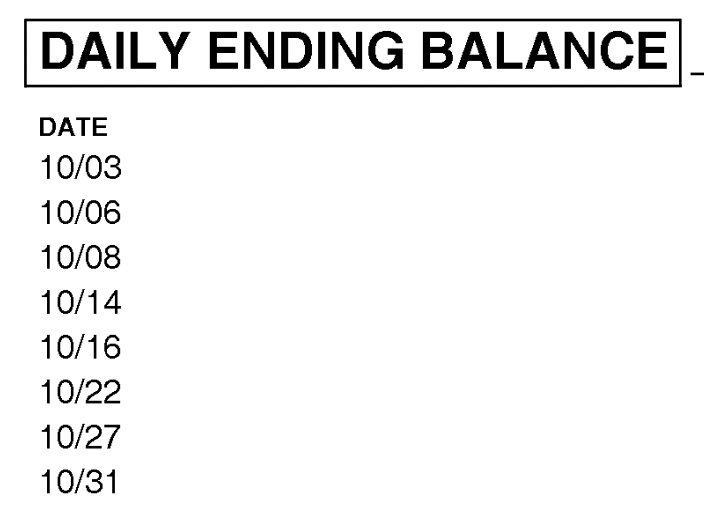

Most banks include a running balance alongside each transaction so you can track the account position after every entry. Chase takes a different approach entirely:

"DAILY ENDING BALANCE." A completely separate section at the end of the statement. It lists the balance at the close of each day, detached from the transactions themselves.

This makes per-transaction verification impossible. You can check the balance at the end of a given date, but if there were five transactions that day, you cannot verify each one individually. For lenders performing detailed cash flow analysis, you need to sum all transactions for each date and compare against the daily balance - which is doable but requires linking data across separate sections of the document. It is exactly the kind of logic that trips up generic extraction tools.

This Page Intentionally Left Blank

And then there is the last page:

"This Page Intentionally Left Blank." That is the entire content of the final page.

It exists for double-sided printing. Chase includes it so the statement does not end with a half-printed back page. Makes sense physically. But a parser processing every page of the PDF will hit this and needs to handle it gracefully - not throw an error because it expected data and found a sentence instead.

Why This Matters for Lenders

Chase statements are not messy. They are actually well organised - just organised differently from everyone else. The separate credit and debit sections, the standalone daily balances, the instance counts in the summary. It is a format designed for reading, not for data extraction.

Parsing a Chase statement correctly means understanding this unique structure: skip the fee notices, extract two separate transaction tables, merge them into one timeline, and reconcile against a daily balance table that lives in its own section. When your lending team receives Chase statements from applicants - which they will, given Chase's market share - they need a tool that handles all of these quirks automatically. A generic tool that does not understand Chase's layout will give you incomplete or jumbled results, and that means unreliable affordability assessments.

ExactSum's Chase-specific parsing logic handles every one of these patterns. Fee notices are filtered out. Credits and debits are merged chronologically. Daily balances are used for verification. Blank pages are skipped. The result is clean, structured transaction data ready for your lending decisions.

Processing Chase Statements for Lending Decisions?

ExactSum handles the quirks automatically so your team can focus on the decision, not the data extraction.

Book a Demo